Investment Thesis

- With double digit growth rates, expansion of cloud kitchens, Amazon backing and the prospect of a unique last mile logistics network, Deliveroo’s IPO is likely to generate significant positive coverage in the coming months.

- We are sceptical given a labour-intensive business model dependent on delivery charges that are under pressure from more profitable incumbents and better funded logistics players.

- A potential valuation >5x estimated FY’20 sales, may not reflect these risks.

Deliveroo could be the UK’s largest IPO in 2021, with over £5bn in market cap speculated to float in April. With double digit growth rates, expansion of cloud kitchens, Amazon backing and the prospect of a unique last mile logistics network, the IPO is likely to generate significant positive coverage. However, our initial thoughts suggest the business is in the squeezed middle. It is under pressure from one side by marketplace incumbents which enjoy stronger profitability, such as Just Eat Takeaway.com and, on the other side, from larger, more ambitious logistics competitors, such as Uber Eats and Delivery Hero. While we are yet to see the IPO prospectus and currently hold no recommendation, the note below elaborates on these preliminary thoughts and why we will continue to work on the name.

Labour Intensive & Unit Economics Dependent on Delivery Charges…

- The company achieved profitability on an ‘operating level’ during 2020 and has remained profitable in the six months leading up to December 2020. However, the COVID-19 impact means this is during a period of arguably inflated average order values, consumer willingness to pay for delivery, and access to labour. Consequently, we question the sustainability of these margins and look forward to further disclosure on the definition of ‘operating level,’ particularly given the -41% and -54% operating margins reported in the 2019 & 2018 statutory accounts (Roofoods Ltd).

- Labour-intensive business model that is facing gig economy scrutiny. Deliveroo’s legal provisions rose >7x between 2018 and 2019 to £32m, with employment rights remaining a contentious issue across its markets. This represents a material reputational and operational risk to the business, given continual negative news flow.

- Unfavourable court rulings: In September 2020, the Spanish Supreme Court ruled that riders for competitor Glovo are employees, not freelancers. This follows a regional ruling in 2019 in Madrid against Deliveroo which also recognised riders as employed and demanded Deliveroo pay social security fees for the contested period. Such court cases are not limited to the classification of riders, but also around the challenges of managing the rider network using technology. For example, a January 2021 judgement in Italy found Deliveroo’s historical rider ranking algorithm discriminatory because it did not allow for legally protected reasons for withholding labour such as sickness or strike action. This exemplifies the complex legal environment Deliveroo must navigate.

- Increasing labour organisation is leading to strikes: A strike in Dublin on 22 January 2021 over allegations of drastically reduced rates of pay, a strike in Hong Kong in May 2020 and one in Paris in August 2019 for similar reasons.

- Competitor action increasing media pressure. Just Eat Takeaway.com (JET) exacerbated this scrutiny by highlighting that Takeaway.com fully employed all its riders and intends to do the same for the combined Just Eat entity across Europe.

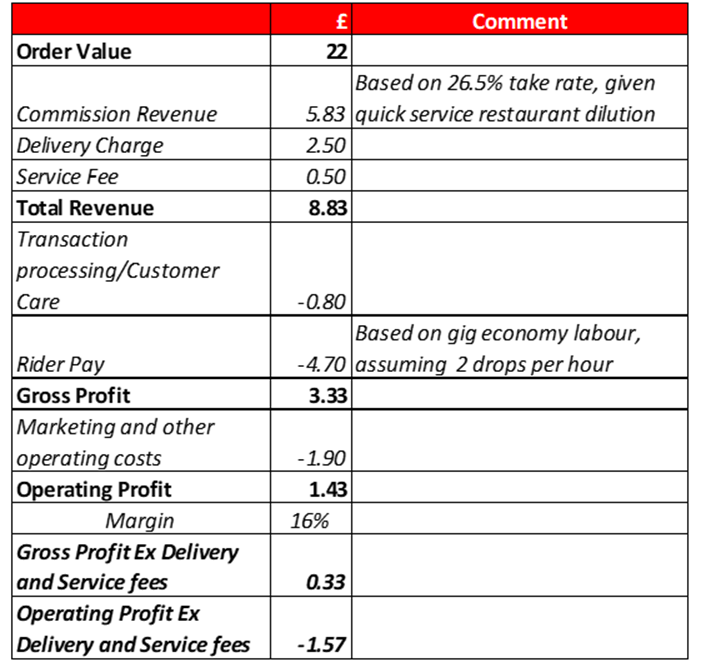

- Unit economics reliant on delivery and service charges. JET’s profitable Canadian business, which is 98% logistics, demonstrates that logistics models can be profitable. However, in Europe, these models face a weaker tipping culture – which is a significant driver of profitability in North America. This places a greater emphasis on delivery and platform charges without which profitability would be unlikely (Exhibit 1).

- In our opinion these charges are not sustainable longer term. Deliveroo’s business largely depends on providing logistics to restaurants who do not typically deliver. Just Eat’s previous reluctance to roll out logistics gave Deliveroo a unique restaurant inventory in key markets and meant if a consumer wanted a particular restaurant meal, few alternatives were available. This is no longer the case, with Uber Eats and JET rapidly expanding their restaurant inventories.

Exhibit 1: Illustrative UK Unit Economics Showing High Dependency on Delivery and Service Charges

Source: The Analyst Estimates

…Which Are Vulnerable Given Market Share Pressure

UK: Competitive Pressure Ramping Up

The UK is Deliveroo’s home and arguably most significant market, generating an estimated 57m orders in 2020, with an ~18% market share. However, the company sits in the squeezed middle, with pressure from the likes of JET and Uber Eats. Both competitors are vying to secure a dominant market share position. This result of this dynamic has caused the following.

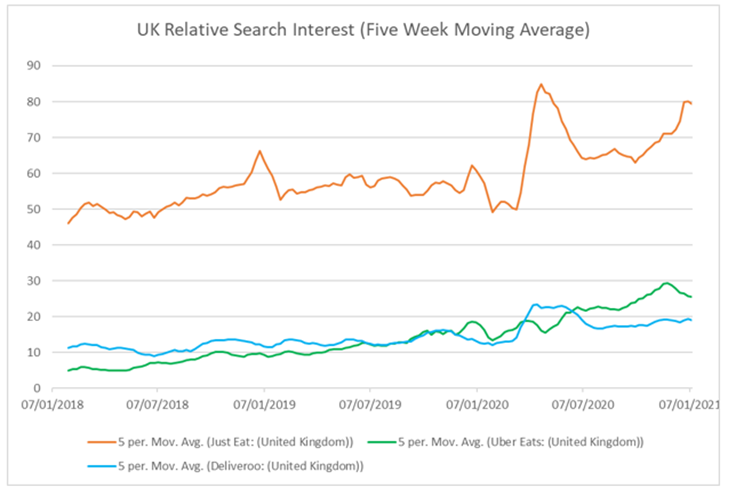

- Deliveroo has lost its No. 2 position in the UK to Uber Eats. Per Exhibit 2, Deliveroo was unable to maintain its market position even before COVID-19. We note this was despite adding grocery orders during 2020, which is likely to skew search interest upwards.

- The core London market is under pressure. Given its high population and restaurant density, London forms the core of Deliveroo’s UK market. While Deliveroo has laid out plans to expand into a further 100 UK town and cities to boost its UK coverage to ~66%, JET’s CEO notes its business is ‘at 100% [coverage] and are going to go after London. And if somebody else wants to go after 100 hamlets, then by all means.’ This is already playing out, with Just Eat announcing free delivery on major chains in London from 18 January 2021, and is rapidly rolling out its own branded logistics offering, Scoober.

- JET UK logistics orders are set to overtake Deliveroo’s total UK orders. JET’s logistics orders in Q4’20 grew 4.9x on Q4’19, resulting in ~6m logistics orders in December 2020 compared to ~7m in total for Deliveroo. Hence, Deliveroo’s logistics capabilities are no longer unique and with that, we expect its unique restaurant inventory to dwindle over time.

Exhibit 2: UK Search Interest Illustrates Deliveroo Overtaken by Uber Eats

Source: Google Trends (Accessed January 2021)

- JET can sustainably offer low or no delivery fees. Despite the ramp up in logistics orders, JET’s UK business was ~75% marketplace in Q4’20. Given the marketplace business can yield >65% estimated adjusted EBITDA margins at scale, the business can indefinitely sustain negative margin logistics orders and still achieve overall UK EBITDA margins >30%.

- JET’s UK operating costs are spread across 2.8x Deliveroo’s total UK orders. This can yield, for example, more efficient national marketing campaigns, vital in an industry where top of mind awareness is a crucial KPI.

- Low fees ignite a positive spiral. JET’s experience in continental Europe highlights that consumers are reluctant to pay delivery fees, meaning players that offer free or cheap delivery experience significantly higher order volumes, in turn attracting more restaurants. For example, despite trialling both Just Eat and Deliveroo for its delivery offering, Greggs rolled out its delivery offer with Just Eat, which we believe was driven by its ability to provide low delivery fees that Deliveroo could not match.

Not the Only Difficult Market Without a No. 1 Position

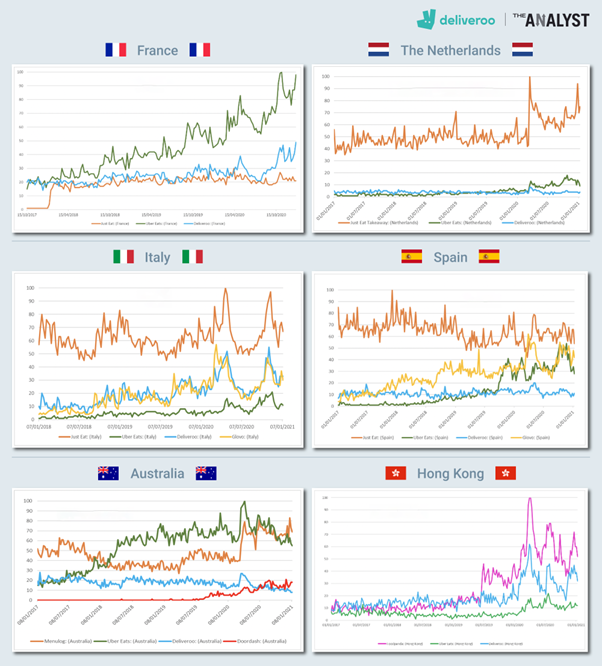

Deliveroo operates in 12 markets in total, with 75% of its FY’19 revenue coming from Europe. Outside of the UK, key markets include France, Italy, Spain, and the Netherlands. The balance of group revenue derives from Kuwait, the UAE, Singapore, Hong Kong, and Australia. Per Exhibit 3, the ‘squeezed middle’ UK problem is replicated in other markets, with no single geography providing a clear market leadership position.

- France. Despite Deliveroo being the earlier mover in France , Uber Eats has gained the dominant market share (Exhibit 3). In Paris, JET recently posted a recruitment manager job vacancy which details a target of recruiting 2000 staff, which we believe points to aggressively rolling out the local logistics offering. Hence, this is another key market for Deliveroo where we believe competitor pressure is ramping up.

- The Netherlands. Deliveroo entered the Netherlands in 2015, yet it has failed to gain material market share against the incumbent, JET, and also lost its No. 2 position to Uber Eats in 2019. This is despite launching its Marketplace+ strategy in 2018 where it added restaurants with their own delivery capacities on its platform in an attempt to compete with Takeaway.com’s marketplace business.

- Spain and Italy. Alongside JET and Uber Eats, Deliveroo also competes with Glovo, an arguably more ambitious Spanish logistics player that delivers across verticals and has launched its own dark store network. Spain is particularly a concern as Deliveroo is now the No. 4 player in the country, down from No. 2.

- Kuwait. This is one of the most attractive food delivery markets globally given high order rates and favourable basket value to labour cost ratios. Delivery Hero’s Talabat brand remains the market leader and we believe is significantly ahead of Deliveroo in utilising its logistics network to facilitate rapid, multi-vertical delivery.

- Singapore & Hong Kong. In both markets, Deliveroo competes with the more ambitious Delivery Hero through its Foodpanda brand, as well as the $14bn SoftBank-backed Grab in Singapore. Deliveroo does not hold the leading position in either market.

- These competitive pressures already led to Deliveroo’s exit in Germany in 2019 and Taiwan 2020.

Exhibit 3: No Clear Leadership Position in Any Key Markets – Deliveroo (Blue), JET (Orange), Uber Eats (Green), Glovo (Yellow), Foodpanda (Pink), DoorDash (Red)

Source Google Trends (Accessed January 2021)

The Ambition: Cloud Kitchens & Multi-Vertical Delivery

We expect the bull case will focus on the roll out of cloud/dark kitchens – commercial kitchens purpose-built for food delivery that eventually may remove restaurants from the value chain – and expansion into delivering non-hot food, including groceries. However, given the competitive dynamics highlighted above, we question whether the business will reach sufficient scale and profitability before competitors build out capabilities in these areas, if desirable.

Cloud kitchens are difficult to get right. In 2019, Uber abandoned its trials of cloud kitchens as part of its measures to focus on profitability. Uber’s ex-CEO also struggled to retain a key collaborator in 2020 for his cloud kitchen business on concerns over the viability of the model. We also highlight that, despite aggressive expansion of its logistics business, Delivery Hero’s Q2’20 update highlighted that cloud kitchens remain a ‘very tough area’ and the company is yet to find sufficient confidence in the business model to aggressively scale it.

Amazon Investment

Given Amazon holds a ~16% stake in Deliveroo, it is appealing to speculate on a potential longer-term takeover and integration into Amazon’s ecosystem given the high order frequencies food delivery can generate. However, we believe such a scenario is unlikely for the following reasons.

- The CMA would likely block a full takeover. The CMA would have the opportunity to review a transaction where Amazon assumed control over Deliveroo. Given the 13 months it took to approve the 16% stake that was only granted over fears Deliveroo may otherwise run out of cash, it is difficult to envisage a full takeover not being held up by anti-trust concerns. We note two previous approaches by Amazon for a takeover were unsuccessful.

- Amazon is just another investor. Amazon’s minority stake and single board seat out of seven suggests it is similar to other financial investors. Without a full merger, we believe other shareholders would be reluctant to allow a competitive strategy that would benefit Amazon at the expense of Deliveroo’s P&L. Ultimately, Amazon’s $575m stake in Deliveroo represents just ~0.03% of Amazon’s market cap, meaning the investment does necessarily commit it to further collaboration with Deliveroo.

Valuation

We are yet to see the 2020 accounts, although Reuters reported that sources stated a likely 2020 revenue range of £800-£1bn. The upper end represents ~30% growth on the 2019 Roofoods statutory accounts and compares unfavourably to 2019’s 62% growth. A fundraising round in January 2021 valuing the business at $7bn (£5.1bn) arguably sets a floor for an IPO valuation, implying a ~5x sales multiple. While transaction multiples from the likes of Takeaway.com in Germany and Delivery Hero in South Korea suggest 8-9x revenue multiples are not outlandish and may provide bulls justification for a higher valuation, we consider Deliveroo a weaker asset given the lack of leading market shares, a dark kitchens offering that is yet unproven, and lower margin potential given a focus on logistics orders. Grubhub, which also has concerns over weakening market share, trades at ~3.5x FY’20e sales and could therefore be a better guidepost for Deliveroo’s valuation.

We look forward to running through the IPO prospectus in the coming months, which may shed more light on unit economics, including that of its cloud kitchens, and 2020 financial data to allow more a more detailed analysis.

Conclusion

Deliveroo could be the largest UK IPO in 2021. With limited options for high growth investors in Europe and ambitions of a unique last mile logistics network, we expect significant positive commentary in the coming months. However, we remain sceptical given a labour-intensive business model that is under considerable competitive pressure in all its markets. We look forward to a formal IPO prospectus to conduct more detailed work on the name.